Written By James McClary, John Mercury and Jon Truswell

Are going private transactions on the rise? Conditions are ripe for an increased number of private equity-led buyouts of public companies.

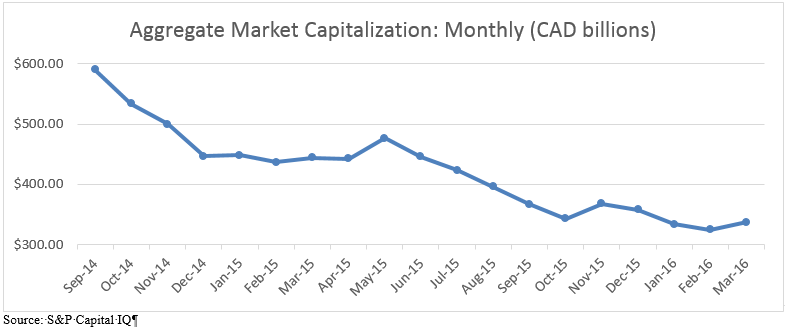

In a "lower for longer" commodity price environment, Canadian energy and energy-services companies are facing difficult circumstances in preserving value. Total declines in market capitalization among Canadian oil and gas companies during the period from July 2014 to February 2016 are estimated to exceed $230 billion, based on available data from S&P Capital IQ (chart below). Management teams have been particularly hard hit: approximately $11.4 billion of those losses are attributable to shares and options held by management and other insiders.

This environment is causing companies to reconsider how they do business. The severity of current and prospective market conditions is forcing them to look beyond conventional means of cost savings, such as reduced G&A, lower operating costs or shutting-in production. Whether as part of a strategic process or otherwise, companies are increasingly looking at more fundamental alternatives in order to preserve enterprise value, with a view to positioning themselves for growth when conditions improve.

One strategic alternative which is attracting attention in the current environment is the going private transaction, where public shareholders are bought out for cash and the company delists and becomes a private, non-reporting company. A going private transaction allows management teams to focus on what they do best – creating value – without the cost and pressures associated with being a public company. This is especially true for companies who are able to partner with a private equity fund or other source of long-term capital, as those types of institutional investors are able to finance and support acquisitions, capital expenditure requirements and working capital/liquidity needs during an extended downturn.

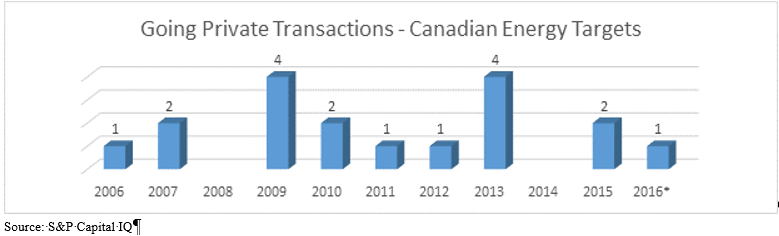

Since July 2015, there have been three private equity-backed going private transactions involving Canadian energy and energy-services companies: Canamax Energy Ltd. (Edge Natural Resources) and Platino Energy Corp. (Denham Capital), both now completed, and Boulder Energy Ltd. (ARC Financial), announced on February 24, 2016. In contrast, there were only 15 going private transactions in the sector during the prior 10 years.

We expect growing interest in going private transactions in 2016 in the energy and energy-services sector of the economy. The reasons for these are several.

First, a number of newly-raised energy-focused private equity funds have closed in recent years, and, as a result, there is significant "dry powder" on the sidelines, both in terms of equity and debt capital, looking for attractive M&A targets. Moreover, the low Canadian dollar may generate additional investment interest by US private equity funds in particular, given that Canadian company valuations may be more attractive in US-dollar terms than comparable US companies.

Second, there is pressure on private equity funds to source new transactions and to back (and thus tie-up) good management teams, especially in areas of the energy sector that are opportune for industry consolidation.

Third, existing management teams in publicly-traded companies whose share price has not reached its potential often find it appealing to partner with a financial sponsor who can not only close the going private transaction, but who will also finance future growth opportunities. This partnership between a financial sponsor and management can also provide the latter with significant economic upside if cash-on-cash returns to the sponsor exceed agreed-upon hurdle rates.

Finally, a growing number of public companies in the commodities space have been running strategic reviews for long periods of time, and, as a result, target board members (and target shareholders) may be more amenable to recommending (or accepting) a cash-out offer made by a private equity fund, if the transaction consideration is found to be fair, from a financial perspective.

Going Private Transactions in a Nutshell

A going private transaction is an M&A transaction led by one or more investors in which public shareholders are bought out for cash and have no continuing equity interest in the resulting private company. Going private transactions may be led and financed by an institutional investor such as a private equity fund (typically in partnership with management), or may be led by management or by a significant existing shareholder.

Public companies choose to go private for a number of reasons. In addition to those noted above, these reasons may include:

- Opportunity to provide liquidity to existing investors;

- Difficulty of raising capital in volatile markets;

- Ability to eliminate legal, compliance and other costs of being a public company and, where applicable, the expectation of paying dividends;

- Increased ability to focus on long-term objectives rather than short-term profits;

- Greater flexibility in structuring governance, compensation and related matters;

- Limited number of attractive strategic alternatives available; and

- Potential to de-lever the balance sheet.

Transaction Considerations

Going private transactions give rise to a number of special considerations, including:

- Managing conflicts of interest;

- Director independence, special committees and engagement of advisors;

- Role of management during due diligence and in negotiations;

- Transaction structure considerations to minimize execution risk;

- Minority shareholder protections; and

- Disclosure obligations.

Going private transactions often come hand-in-glove with conflicts of interest, especially where management is supportive of the financial purchaser. Given the enhanced scrutiny such transactions receive from shareholders, regulators and proxy advisory firms, such considerations are best addressed by the board of directors (and special committees) with outside legal and financial advisors at the outset. A well-designed and documented process will help the board and management discharge their fiduciary duties and lead to a successful outcome for all parties.

Private Equity Structure Considerations

For transactions sponsored by a private equity fund (the Canamax, Platino and Boulder transactions were all PE-sponsored), there are a number of additional considerations, including:

- Post-closing structure of the investment, including legal and tax considerations;

- Management rollover of existing equity or options and reinvestment in the business;

- Shareholder/partnership agreements, which raise a variety of complex issues surrounding governance, financing and liquidity rights, including restrictions on transfer;

- Employment arrangements for management; and

- Management equity incentive structures.

Private equity funds will typically have their own customized approach to these issues. Management teams would be well-served to engage legal advisors that are well-versed in advising management teams and private equity funds with respect to these matters.

Bennett Jones LLP has significant experience representing both management teams and private equity investors in going private transactions. We are available to meet confidentially with interested parties to discuss in a detailed presentation the considerations outlined above. For further information please contact any one of our experienced lawyers, including:

John Mercury: 403-298-4493 / mercuryj@bennettjones.com

Jon Truswell: 403-298-3097 / truswellj@bennettjones.com

James McClary: 403-298-3651 / mcclaryj@bennettjones.com

Please note that this publication presents an overview of notable legal trends and related updates. It is intended for informational purposes and not as a replacement for detailed legal advice. If you need guidance tailored to your specific circumstances, please contact one of the authors to explore how we can help you navigate your legal needs.

For permission to republish this or any other publication, contact Amrita Kochhar at kochhara@bennettjones.com.